In the dynamic world of entrepreneurship, the question arises: Can a woman get a business loan? Absolutely, and the landscape is evolving. Business loans for women have emerged as a vital catalyst for economic development, promoting gender equality. Governments globally are acknowledging the imperative to uplift women in business. This article delves into the intricate details of business loans for women, exploring government initiatives, challenges, and the key to overcoming hurdles with Prudent Capital.

What is a Business Loan for Women?

A business loan for women is a strategic financial tool designed explicitly for female entrepreneurs aiming to establish or expand their ventures. Tailored features, including flexible repayment terms, lower interest rates, and additional support services, acknowledge the unique challenges and opportunities faced by women-led businesses.

Business Loans for women from the government

Governments worldwide have introduced initiatives to encourage women’s entrepreneurship, aiming to bridge the gender gap in business ownership. These inclusive programs create a more diverse and equitable economic landscape, offering business loans for women without collateral through various schemes.

Key Benefits for Women Entrepreneurs

Business loans for women extend beyond providing financial support. They empower women entrepreneurs, offering a capital injection that translates into confidence, independence, and a platform to showcase their skills. Inclusive policies adopted by governments pave the way for gender diversity across various industries.

Challenges Faced by Women in Business Loans

Despite positive strides, women encounter hurdles in securing business loans. Discrimination, gender bias, and limited awareness about available options persist as challenges. Breaking down these barriers is crucial to creating a level playing field for women in the entrepreneurial landscape.

Why Prudent Capital’s Business Loans for Women?

Navigating the challenges of securing a business loan as a woman entrepreneur is made easier with Prudent Capital. Our tailored business loans are designed to address the specific needs and challenges faced by women in business. Here’s how we can help you overcome hurdles:

No Collateral Required: Prudent Capital understands the hesitation around pledging assets. Our business loans for women require no collateral, ensuring a more accessible and flexible financing option.

Quick Approval: In the fast-paced world of business, time is a critical factor. Wondering where to get fast approval for business loans for women? Look no further than Prudent Capital. With us, experience swift approval processes, getting you the funds you need in a timely manner.

Low-Interest Rates:Find the best rates on business loans for women with us. We present competitive interest rates, making our business loans an economically sound solution for women entrepreneurs.

Flexible Repayment Terms: Tailor the repayment terms to align with your cash flow and financial situation, providing you with the flexibility needed to succeed.

What are the Eligibility criteria for women to get business loans?

To qualify for our business loans, aspiring women entrepreneurs should meet the following criteria:

Age Requirement: Above 21 years

Business Vintage: 1 year and beyond

Credit Score: A minimum credit score of 700 is necessary

At Prudent Capital, eligibility is not a hurdle; it’s an invitation to unlock new possibilities. Get approved for business loans for female-owned startups and take the first step towards realizing your entrepreneurial dreams.

Your Journey with Prudent Capital

Prudent Capital is not just a financial partner; we are committed to empowering women in business. Our business loans serve as more than a financial support system – they are a catalyst for your success in the entrepreneurial world. Choose Prudent Capital and take the next confident step toward achieving your business goals. Empowerment begins here.Get funding for your women-owned business today!

FAQ

1.Is it possible for women to secure a business loan?

Certainly! If you’re a woman with a business, explore the option of a business loan designed for women in India with Prudent Capital.

2. Which financial institution provides rapid approval for startups led by women?

Prudent Capital stands out as a reliable choice, offering swift approval processes tailored explicitly for women-led startups.

3. How can a woman apply for a business loan?

Securing a business loan with Prudent Capital is quite simple. Just head to ourcontact page, fill out the user-friendly form and Ensure you have essential documents like business details, financial statements, and identification ready. Our efficient process guarantees a prompt review, providing women entrepreneurs with the financial support they need for their small businesses.

Are you a new business owner looking to advance your venture?

As much as you have the super hyper motive to start your very own venture you must surely understand the importance of having access to initial capital or startup capital. That’s where MSME loans come in. These loans cater to Micro, Small, and Medium Enterprises, providing them with the financial boost they need to thrive in today’s competitive marketplace.

Whether you want to expand your operations, upgrade equipment, or invest in new technology, MSME loans can unlock the potential of your business. With flexible repayment terms and competitive interest rates, these loans offer a lifeline to entrepreneurs who may not qualify for traditional business loans, however there are certain criteria to be met and that’s what you will be reading in this comprehensive guide.

Securing an MSME loan gives you the financial stability to fuel growth, hire skilled talent, increase your market share and it truly is a chance to propel your business towards success.We atPrudent Capital are aware of the various financial requirements that companies have. While there are many types of business loans such as MSME loans,Working Capital loans, term loans, loan against property, business loans for women, and unsecured loans it can become quite daunting for a new business owner to find out which one could suit their business needs and which loan they could be approved for by the banks or NBFC’s.

Prudent Capital offers specialised financial consulting services to help you navigate the complexities of obtaining the best MSME financing for your particular business endeavour.

Never allow a shortage of funds to impede your progress. Refrain from being hindered by financial constraints and forge ahead towards your goals. Discover the transformative power of MSME loans and unlock the potential of your new business today.

Understanding the importance of MSME loans for new businesses

Starting a new business is an exciting endeavour, but it’s challenging. One of the biggest hurdles new entrepreneurs face is the lack of funds to fuel growth and expansion. Traditional bank loans often have strict eligibility criteria and high interest rates, making them unattainable for many small businesses. This is where MSME loans play a crucial role. They are designed to meet small and medium enterprises’ unique needs, offering flexible repayment terms and competitive interest rates.

MSME loans provide new businesses with the opportunity to access the funds they need to

– Expand their operations: Whether you want to open a new location, increase your production capacity, or enter new markets, MSME loans can provide the financial stability required to fuel growth.

– Upgrade equipment: Keeping up with the latest technology and equipment is essential for staying competitive. MSME loans can help you invest in state-of-the-art machinery and tools to streamline operations and improve efficiency.

– Invest in new technology: In today’s digital age, businesses must adapt to technological advancements to stay ahead. MSME loans can help you invest in software, hardware, and other technical solutions to enhance your productivity and customer experience.

Types of MSME loans offered by Banks & NBFC’s

Regarding MSME loans, several options are available to suit the specific needs of different businesses. Here are some of the most common types of MSME loans:

1. Working Capital Loans: These loans cover day-to-day operational expenses such as inventory, salaries, and marketing. They provide businesses with the cash flow to keep their operations running smoothly.

2. Term Loans: Term loans are typically used for capital expenditures such as purchasing equipment, expanding infrastructure, or renovating premises. They come with fixed repayment terms and allow businesses to repay the loan over a specified period.

3. Equipment Financing: This type of loan is specifically designed to help businesses purchase or lease equipment. Whether you need to buy new machinery or upgrade your existing equipment, equipment financing loans can provide the necessary funds.

4. Trade Finance: Trade finance loans are ideal for businesses involved in import-export activities. These loans help manage the cash flow gap between paying suppliers and receiving payments from customers.

Eligibility criteria for MSME loans

There are somefactors considered by banks in approving business loans. Businesses must meet specific eligibility criteria. While the exact requirements may vary depending on the lender, here are some common factors considered:

1.Business Vintage: Most lenders prefer businesses with a minimum operational history of 1-3 years. This helps establish the credibility and stability of the business.

2. Annual Revenue: Lenders typically look for a minimum annual turnover to ensure the business can repay the loan. The specific revenue requirement may vary based on the loan amount and type.

3. Credit Score: A good credit score is crucial for loan approval. Lenders assess the business’s creditworthiness by evaluating its repayment history and credit utilisation.

4. Business Plan: Lenders may require a detailed business plan outlining the objectives, financial projections, and repayment strategy. This helps them assess the viability and potential of the business.

Explore a comprehensive understanding of what lies ahead:

1. Investigate and contrast lenders: Initiate your journey by delving into diverse lenders, meticulously examining and contrasting the loan options they extend.

2. Gather documents: Each lender will have specific document requirements, but standard documents include proof of identity, address, business registration, financial statements, and tax returns. Ensure that you have prepared all essential paperwork before submitting your application.

3. Fill out the application form: Once you’ve chosen a lender, fill out the loan application form. Furnish precise and comprehensive details to prevent any hindrances in the approval procedure.

4. Submit the application: Apply with the required documents to the lender. Some lenders may also accept online applications, making the process more convenient.

5. Loan evaluation and approval: The lender will evaluate your application, review the submitted documents, and assess your eligibility.

The duration of this procedure can vary from several days to a few weeks, contingent upon the internal processes of the lending institution.

6. Loan disbursement: If your loan is approved, the lender will disburse the funds to your designated bank account. Carefully review the loan agreement and repayment terms before accepting the funds.

Benefits of MSME loans for new businesses

MSME loans offer numerous benefits to new businesses, giving them a competitive edge in the market. Here are some key advantages:

1. Access to Capital: The primary benefit of MSME loans is their access to capital. Whether it’s for working capital needs, expansion plans, or technology upgrades, these loans bridge the gap between business aspirations and financial constraints.

2. Flexible Repayment Terms: Unlike traditional bank loans, MSME loans often have flexible repayment terms. This allows businesses to customise their repayment schedule based on their cash flow and revenue projections.

3. Competitive Interest Rates: MSME loans typically offer competitive interest rates compared to other forms of financing. This ensures that businesses can manage their loan repayments without burdening their profitability.

4. Faster Approval Process: With the advent of digital platforms and online loan applications, the approval process for MSME loans has become faster and more streamlined. This means businesses can access funds quickly and seize growth opportunities without delay.

5. Credit Building: Successfully repaying an MSME loan can help businesses build a positive credit history, making securing future funding from banks and other financial institutions easier.

Common challenges faced when applying for MSME loans

While MSME loans offer numerous advantages, businesses may face some common challenges during the application process. It’s essential to be aware of these challenges and plan accordingly. Some of the main challenges include:

1. Strict Eligibility Criteria: Meeting the eligibility criteria set by lenders can be challenging, especially for new businesses with a limited financial history. It’s crucial to thoroughly research the requirements of different lenders and choose the one that aligns with your business profile.

2. Documentation Requirements: MSME loan applications often require extensive documentation. Ensuring all the documents are in order and up to date can be time-consuming and tedious. It’s advisable to maintain organised records and keep them readily accessible.

3. Collateral Requirements: Some lenders may require collateral as security against the loan. This can be a challenge for businesses that do not have substantial assets to offer as collateral. Exploring lenders that offer unsecured MSME loans can be a viable alternative.

4. Limited Loan Amounts: MSME loans may have limitations on the maximum loan amount available. It’s essential to carefully assess your funding requirements and choose a lender that can provide the necessary funds to meet your business goals.

Tips for maximising the potential of MSME loans

To make the most of an MSME loan, here are some tips to keep in mind:

1. Plan Ahead: Before applying for an MSME loan, have a clear plan in place. Define your business goals, identify the areas where you need financial assistance, and estimate the required loan amount.

2. Research Multiple Lenders: Don’t settle for the first lender you come across. Research multiple lenders, compare their offerings, and choose the one that best suits your business needs. Seek out lenders offering advantageous interest rates, repayment conditions, and positive customer feedback.

3. Prepare Comprehensive Documentation: To expedite the loan approval process, ensure all required documentation is complete and accurate. This includes financial statements, tax returns, business plans, and any other documents the lender requests.

4. Maintain a Good Credit Score: A good credit score is crucial for loan approval. Make timely payments on existing debts, keep credit utilisation low, and regularly monitor your credit report for any discrepancies.

5. Create a Repayment Plan: Create a repayment plan that aligns with your business’s cash flow before accepting the loan. This will help you stay on track with your loan repayments and avoid financial strain.

Conclusion: Empowering new businesses with MSME loans

Embarking on a novel business venture marks a thrilling odyssey brimming with both prospects and obstacles. The inception of a new business not only opens doors to exciting possibilities but also presents a landscape rife with diverse challenges. Access to capital is crucial for fueling growth and turning business dreams into reality. MSME loans provide new businesses with the financial stability needed to expand operations, invest in technology, and hire skilled talent.

By understanding the significance of MSME loans, exploring the available types, and successfully navigating the application process, entrepreneurs can unlock the true potential of their new businesses.

Though challenges may arise during the loan application process, maintaining organised documentation, researching multiple lenders, and ensuring a good credit score can help overcome these hurdles. For a better understanding, it is always a good idea to contact an expert in the field and you can contact Prudent Capital 24/7.

Don’t let a shortage of funds hinder your progress. Discover the transformative power of MSME loans and unlock the potential of your new business today.

FAQ

1.Are MSME loans exclusively designed for established businesses, or can startups also benefit?

MSME loans are designed to serve the needs of both established businesses and startups alike. For businesses with less than one year of operation, providing suitable collateral or a guarantee from an individual with a high annual turnover and good credit score may increase the chances of securing an MSME loan. These loans become a pivotal resource for startups, empowering them to initiate growth and navigate the initial hurdles of financial challenges.

2.How quickly are MSME loans approved and funds disbursed?

With the streamlined efficiency of digital processes, MSME loan approvals typically take days to a few weeks. At Prudent Capital, count on us for swift approvals and rapid fund disbursement to meet your business requirements promptly.

3.Who qualifies for MSME loans at Prudent Capital?

Any registered business both self-employed professionals and self-employed non-professionals can apply for MSME loans. This inclusivity means that individuals such as retailers, proprietors, traders, and others have seamless access to MSME loans.

In the ever-evolving business realm, obtaining optimal financing can be transformative. One notable avenue that has proven beneficial for many entrepreneurs is the secured business loan. A secured business loaninvolves borrowing money backed by collateral. This collateral could be real estate, equipment, or other valuable assets owned by the business or the borrower.

This collateral serves as a safety net for the lender, reducing the risk and, in turn, leading to more favourable terms for the borrower. These loans are crucial in providing financial stability and opportunities for business growth. By understanding the nuances of secured loans, entrepreneurs can make informed decisions about their financial future.

Benefits of Secured Business Loans

A. Lower Interest Rates

One significant advantage of secured loans is the lower interest rates compared to unsecured alternatives. Lenders see secured loans as less risky due to the collateral, resulting in cost savings for the borrower.

B. Higher Loan Amounts

Secured loans often allow businesses to secure higher loan amounts, providing access to more substantial capital for expansion, equipment purchase, or other strategic initiatives.

C. Longer Repayment Terms

The extended repayment terms of secured loans offer businesses flexibility in managing their cash flow. This proves especially advantageous in times of economic adversity.

D. Easier Approval Process

Securing a loan with collateral can streamline the approval process, making it easier for businesses to access the funds they need. This is especially advantageous for those with less-than-perfect credit.

Eligibility Criteria for Secured Business Loans

A. Credit Score Requirements

While secured loans are more forgiving of lower credit scores, a reasonable credit history is still essential. Lenders might consider both the individual’s credit score and the credit score associated with their business. A credit score of 750 and above is typically preferred for favourable loan terms.

B. Business Financial Stability

Lenders assess the business’s financial stability, looking at factors such as revenue, profitability, and overall financial health. A business vintage of over one year is often a positive indicator.

C. Collateral Assessment

The value and type of collateral are critical factors in determining loan eligibility and terms. Lenders will thoroughly assess the collateral to ensure it aligns with the loan amount.

Documents Required for Secured Business Loans

A. Personal and Business Documentation

Applying for a secured loan involves providing documentation such as personal and business tax returns, financial statements, and legal business documents.

B. Collateral Documentation

Detailed collateral documentation, including appraisals and ownership verification, is crucial for the loan application process.

C. Business Plan

A well-structured business plan showcases the borrower’s vision, strategy, and how the loan will contribute to achieving business objectives.

Tips for Securing a Favourable Loan

A. Improving Credit Score

Taking steps to improve personal and business credit scores can enhance eligibility for better loan terms.

B. Choosing the Right Collateral

Carefully selecting collateral that aligns with the business’s needs and has significant value can positively impact loan terms.

C. Negotiating Loan Terms

Negotiating with lenders can result in more favourable terms, such as lower interest rates or extended repayment periods.

In Summary, a secured business loan can be a valuable asset for businesses seeking financial stability and growth. By understanding this, entrepreneurs can make informed decisions that align with their strategic objectives. Empowering businesses to make informed decisions about financing options is essential. Secured loans, when utilised strategically, can pave the way for sustained success.

FAQ

How long does the approval process for a secured loan usually take?

The approval process varies among lenders, but securing all necessary documentation and having a well-prepared application can expedite the process.

2. Is a secured business loan the right choice for every business?

Secured loans benefit many businesses, but their suitability depends on individual circumstances. Consulting with financial advisors can provide personalised insights.

3. Why take a secured business loan from Prudent Capital?

Prudent Capital offers appealing secured business loans tailored to your business requirements. Benefit from competitive interest rates, swift loan approval, and a streamlined documentation process for your convenience.

Embarking on the journey of starting a new business requires careful financial planning, and exploring diverse funding options is crucial. Among these, Loan Against Property (LAP) stands out as a noteworthy financial product that allows individuals to leverage the value of their property to secure a loan. The property, which can be residential or commercial, serves as collateral, providing lenders with security and borrowers with access to substantial funds. LAP is often considered a viable option for those seeking significant loan amounts for various purposes, such as business expansion, debt consolidation, or other financial requirements.

Loan against property eligibility criteria

To qualify for a Loan Against Property, applicants must meet specific eligibility criteria set by lenders. These criteria may vary slightly among financial institutions, but the fundamental factors typically include:

Property Ownership and Type

To be eligible for a LAP, the applicant must own the property they intend to mortgage. The property can be residential or commercial, but its legal title and ownership should be clear. Lenders prefer properties with a clear title, free from any encumbrances.

Age of the Applicant

The age of the borrower plays a crucial role in LAP eligibility. Lenders typically set a minimum and maximum age limit for applicants. Younger individuals may be perceived as having a longer repayment tenure, while older individuals may face restrictions due to potential income uncertainties during the loan tenure.

Income Stability and Source

Lenders assess the applicant’s income stability and source to evaluate their repayment capacity. Regular employment or a steady income from a business is often preferred. Income documentation, such as salary slips, income tax returns, or business financial statements and GST may be required to verify the applicant’s financial stability.

Credit Score

A good credit score enhances the borrower’s credibility and increases the chances of loan approval. Lenders typically look for a credit score above a specified threshold, reflecting a history of timely payments and responsible credit behaviour. A lower credit score may result in a higher interest rate or even rejection of the loan application.

Loan Amount and Property Valuation

The loan amount sanctioned is directly linked to the valuation of the property. Lenders conduct a thorough assessment of the property’s current market value to determine the loan amount. The Loan-to-Value (LTV) ratio, expressing the loan amount as a percentage of the property’s value, varies among lenders.

Employment or Business Stability

Lenders prefer applicants with a stable employment history or a well-established business. Employment continuity or business stability is indicative of a consistent income source, reducing the risk of default. Frequent job changes or recent business startups may be viewed less favourably.

Debt-to-Income Ratio

The debt-to-income ratio assesses the applicant’s ability to manage additional debt. Lenders consider existing loan obligations, if any, along with the proposed LAP instalment. A lower debt-to-income ratio signifies better financial health and repayment capacity.

Legal and Technical Due Diligence

Lenders conduct legal and technical due diligence on the property to ensure its authenticity and compliance with legal requirements. This includes verifying property documents, conforming land use, and assessing the property’s structural integrity. Any discrepancies may affect the loan approval process.

Residential Status

The applicant’s residential status can impact LAP eligibility. Non-resident Indians (NRIs) may face additional documentation requirements and could be subject to different terms and conditions. Lenders may have specific policies for NRIs seeking a loan against property.

Insurance Requirements

Some lenders may require the borrower to take insurance coverage for the mortgaged property. This aids in risk mitigation for both the borrower and the lender Insurance requirements may vary, but property insurance is commonly mandated to protect against unforeseen events.

In summary, meeting these eligibility criteria enhances the chances of securing a Loan Against Property. Borrowers should be prepared to provide comprehensive documentation and fulfil the lender’s requirements to facilitate a smooth application process. It is advisable for applicants to thoroughly understand the eligibility criteria of the chosen financial institution and address any potential concerns before applying for a LAP.

FAQ

1.Can I get a loan against property with a low cibil score?

Securing a loan against property with a low CIBIL score is challenging, but options exist:

Shop Around: Explore lenders with varying criteria for lower credit scores.

Collateral Value: A property with high value may enhance approval chances.

Higher Costs: Expect higher interest rates or less favorable terms.

Reduced Loan Amount: Lenders may offer a lower loan amount.

Co-Signer or Guarantor: Having a co-signer with a good credit score improves approval odds.

Credit Score Improvement: Work on enhancing your credit score before applying.

Remember the risks involved, and consult financial experts for personalised advice based on your situation and needs.

2.Is loan against property taxable?

In most cases, a loan against property is not taxable as it is considered a loan, not income. However, there are exceptions:

Interest deduction: If used for business, the interest may be tax-deductible with proper documentation.

Rental income: Income from a rented property is taxable, but the loan itself isn’t.

Capital gains: Selling the property may have capital gains tax implications based on local laws and loan use.

Consult a tax professional or financial advisor for region-specific advice, as tax laws vary.

3.What makes opting for a Loan Against Property more advantageous than choosing a standard personal loan?

In contrast to a regular personal loan, a Loan Against Property offers a substantially higher loan amount and a significantly lower interest rate.

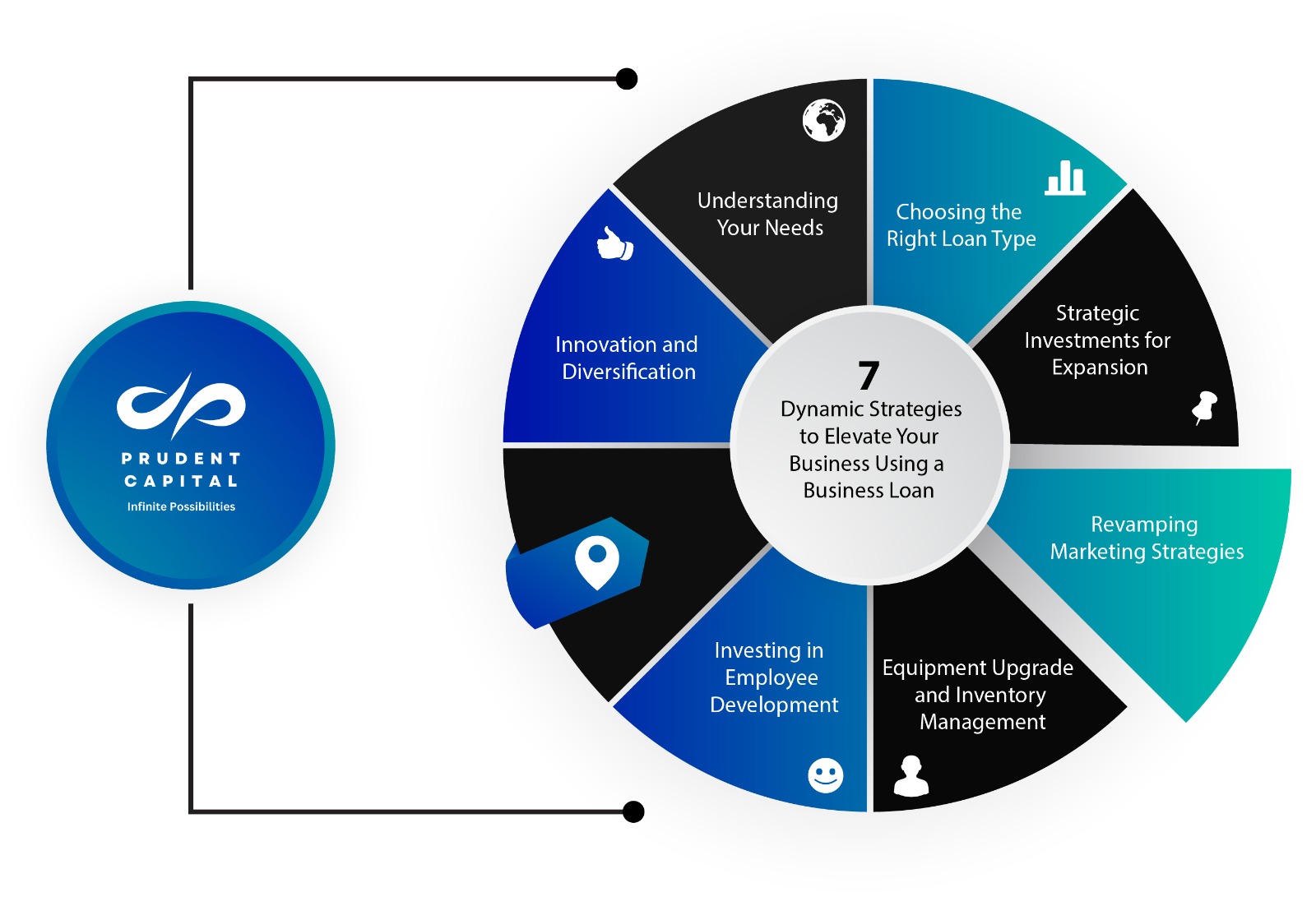

Every entrepreneur knows that fuelling growth often requires financial backing. For those over 50 years in business, navigating the business landscape can present unique challenges, and leveraging a business loan can be a game-changer. Let’s explore seven powerful ways to harness the potential of a business loan to propel your enterprise to new heights.

1. Understanding Your Needs

Before diving into the loan market, introspect! What does your business truly need? Whether expanding your market reach, upgrading equipment, or investing in marketing, identifying your specific requirements sets the stage for a focused loan application.

2. Choosing the Right Loan Type

With various loan options available, finding the one that aligns with your business goals is crucial. Consider the diverse range, from traditional term loans to lines of credit and SBA loans. Each type caters to different needs, so pick wisely to ensure it complements your objectives.

3. Strategic Investments for Expansion

Expanding your business footprint could be a game-changer. Whether opening new branches, entering untapped markets, or broadening services, a well-timed investment using the loan can significantly boost your clientele and revenue streams.

4. Revamping Marketing Strategies

Investing in marketing breathes life into your brand. Embrace digital marketing strategies tailored to your target demographic. A loan could fuel a robust online presence, driving more traffic and conversions. Remember, visibility translates into business growth.

5. Equipment Upgrade and Inventory Management

Efficient tools and well-managed inventory streamline operations. Upgrading equipment or adopting new technologies enhances productivity and quality. Moreover, managing inventory effectively with the help of a business loan ensures you meet increased demand without hiccups.

6. Investing in Employee Development

Your team is the backbone of your business. Empower them through skill development programs. Whether it’s training for new technologies or fostering leadership skills, a business loan invested in your workforce ultimately contributes to enhanced productivity and innovation.

7. Innovation and Diversification

Staying ahead in the market often requires innovation and diversification. Research and development initiatives, backed by a business loan, could lead to new product lines or service offerings. Embracing innovation ensures your business remains relevant and resilient in a constantly evolving landscape.

Embracing Financial Management for Success

While the prospect of a business loan is exciting, prudent financial management is key. Plan meticulously on utilising the loan amount and establish a clear repayment strategy. Seek advice from financial advisors to ensure sound financial decisions. Additionally, knowing the factors banks consider while approving business loans can be a lifesaver in navigating the loan approval process.

In conclusion, a business loan, when utilised strategically, can catalyze substantial business growth. Assess your business needs, explore loan options, and chart a roadmap for leveraging the loan effectively. Remember, it’s not just about the funds; it’s about the smart utilisation that sets your business on a trajectory towards success.

Understanding the Diverse Landscape of Business Loans

In entrepreneurship, securing financing is often crucial Fin fueling business growth and development. However, navigating the many business loan options available can take time and effort. Understanding the types of business loans and their unique advantages can be a game-changer for business owners seeking financial support. Let’s dive into the diverse landscape of business loans:

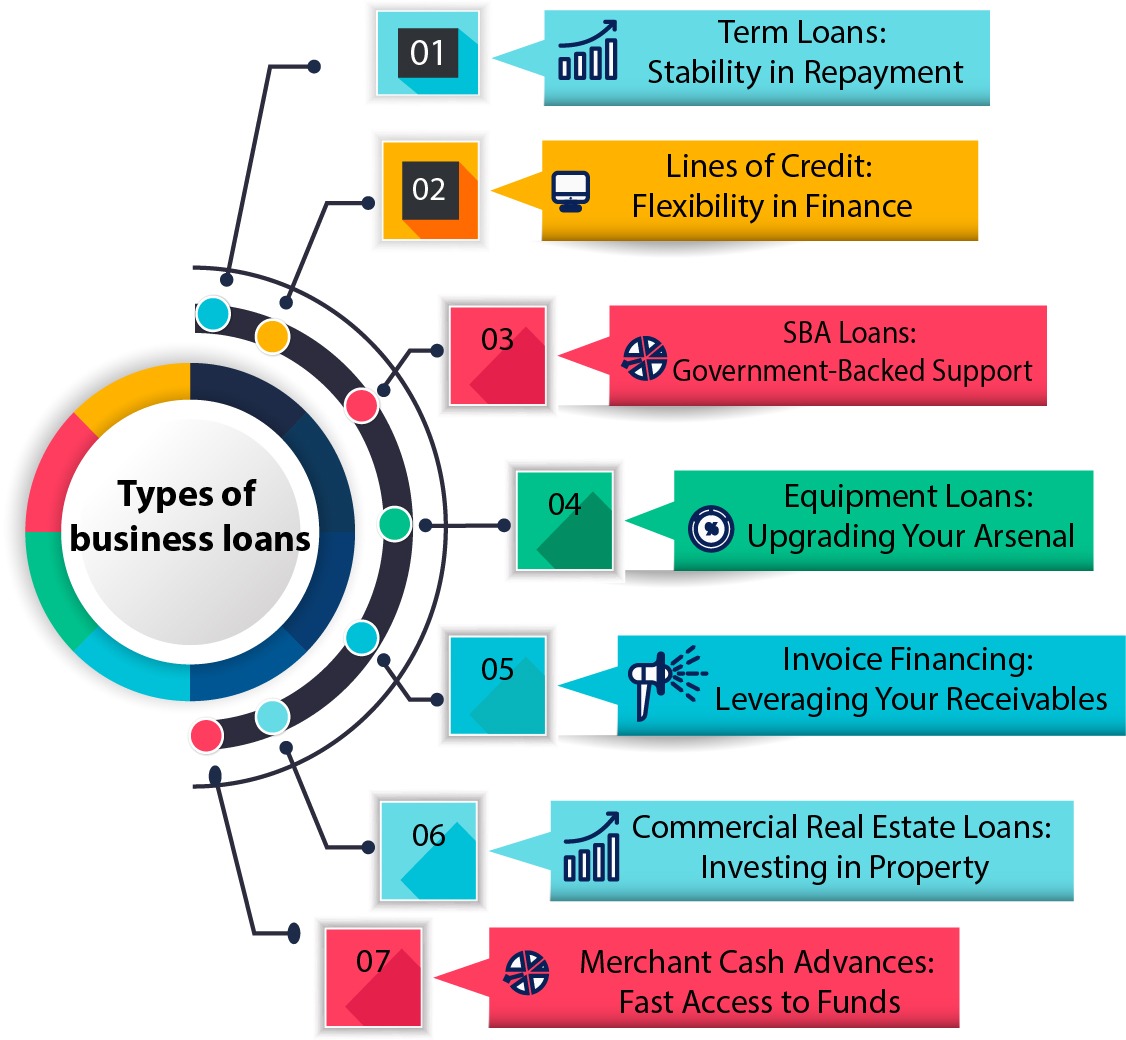

Types of Business Loans

1. Term Loans: Stability in Repayment

Term loans are the most sorted type of business loans among business owners. They involve borrowing a lump sum of money repaid over a predetermined period, usually with a fixed interest rate.

When to Consider: Ideal for substantial investments like equipment purchase, expansion, or hiring. They provide stability in repayment, making it easier to budget.

2. Lines of Credit: Flexibility in Finance

What They Are: A line of credit offers a flexible borrowing option where a lender approves a maximum credit limit. Businesses can withdraw funds as needed and pay interest only on the amount used.

When to Consider: Useful for managing cash flow fluctuations, covering short-term expenses, or taking advantage of unforeseen opportunities without committing to a lump sum loan.

3. SBA Loans: Government-Backed Support

What They Are: Small Business Administration (SBA) loans are partially guaranteed by the government, reducing the risk for lenders. They offer longer repayment terms and competitive rates.

When to Consider: Best suited for businesses with less access to traditional financing or those seeking longer-term loans with lower down payments.

4. Equipment Loans: Upgrading Your Arsenal

What They Are: These loans are designed to purchase equipment or machinery. The equipment itself serves as collateral, often leading to more favourable terms.

When to Consider: Equipment loans offer a specialised solution if you want to upgrade or replace equipment without impacting cash flow.

5. Invoice Financing: Leveraging Your Receivables

What It Is: Also known as accounts receivable financing, this option involves using unpaid invoices as collateral to secure a loan. Lenders advance a percentage of the invoice value and collect once customers pay.

When to Consider: If your business faces cash flow gaps due to slow-paying customers, invoice financing can provide immediate access to funds tied up in invoices.

6. Commercial Real Estate Loans: Investing in Property

What They Are: Tailored for purchasing or renovating commercial properties. These loans typically have longer terms and lower interest rates than commercial loans.

When to Consider: These loans offer property acquisition or development financing if you’re expanding your business space or investing in real estate.

7. Merchant Cash Advances: Fast Access to Funds

What They Are: A lump sum of cash provided upfront in exchange for a percentage of future credit card sales. Repayment is made through a percentage of daily sales.

When to Consider: If you require quick access to funds without a stringent credit check, merchant cash advances offer speedy financing.

Choosing Wisely for Business Success

Selecting the correct type of business loan requires a deep understanding of your business’s financial needs and goals. Each loan type comes with its own set of advantages and considerations. Evaluating the terms, interest rates, repayment options, and eligibility criteria is crucial before deciding.

Remember, while loans can provide essential financial support, responsible borrowing and sound financial planning are paramount. Assess your business’s requirements, explore options, and choose a loan that aligns with your long-term growth strategy.

In conclusion, the diversity in business loan offerings caters to the varied needs of entrepreneurs. By leveraging the correct type of loan at the right time, businesses can propel themselves towards success and sustainable growth.

FAQ

1.How should a business get a business loan from banks or NBFC?

Prudent Capital streamlines the process by leveraging our extensive network with major banks. We ensure a smooth application approval process, focusing on your unique business needs.

2.How should a startup business get a business loan from banks or NBFC?

Startups often face unique challenges, and we understand that. Our approach involves providing tailored solutions for startups, emphasising business plans, and assisting in establishing a solid foundation to boost loan approval.

3.What are the prevalent interest rates on business loans?

Each firm is unique and has a distinct goal. Prudent Capital is dedicated to obtaining competitive interest rates, although they may differ at times.Our tie-ups with major financial institutions enable us to negotiate favourable terms, ensuring your business thrives economically.

6 Benefits of Loan Against Property you need to know

A loan seeker needs to know the features and benefits of the loan type they are looking to avail so that they can compare the advantages against other available loans.

Taking a secured loan against property is far more beneficial when compared to unsecured loans like personal loans, term loans and loan against credit cards. There are many types of secured loans however we are going to gain knowledge on Loan Against Property.

The loan seeker can mortgage a clear title property self-owned or jointly owned commercial or residential to avail a loan against that property. The bank extends a loan equivalent to the property value at the time of mortgage.

Why should a loan seeker opt for a Loan against property?

Are there any special benefits to the loan seeker when LAP is availed?

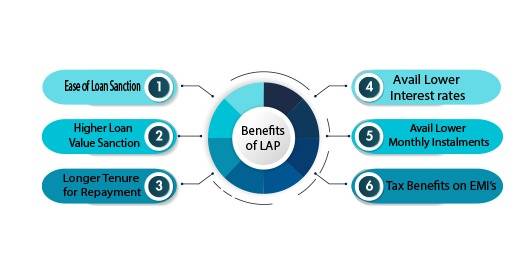

We have listed the top 6 benefits of LAP – Loan against property

Ease of Loan Sanction

Higher Loan Value Sanctioned

Longer Tenure for Repayment

Avail Lower Interest rates

Avail Lower Monthly Instalments

Tax Benefits on EMI’s

Ease of Loan Sanction

Banks and NBFC’s are highly motivated and enthusiastic when it comes to offering loans against property. Loans against property actually puts the lenders in a safe position in fact it also safe guards the borrower. If all paperwork is in place and accurate the banks and NBFC’s will sanction the loans quite easily and quickly.

Higher Loan Value Sanctioned

Loan seeker need to plan their loan journey and, in this way, they can plan the entire tenure and stick to the plan which helps them to repay without any hassle and also plan closure quite comfortably. Banks are quite happy a high value loan based on the property value so that they loan can satisfy few objectives and requirements.

Longer Tenure for Repayment

For Loan Against Property that falls under the secured loan category, the banks willingly offer longer repayment tenures. The maximum repayment tenure with nationalized banks and top banks is 15 years however in some special cases it can be extended up to 20 years and that is left to discretion of the authorities of the banks and NBFC’s.

Avail Lower Interest rates

Lending institutions are willing to offer the advantage of lower interest rates to the loan against property borrowers. The banks in most cases offer a variable low interest rates and in some rare cases they offer fixed interest rates.

Avail Lower Monthly Instalments

Banks and NBFC’s always try to increase offering secured loans as against to unsecured loans. It positions both the banks and the consumer on a safe loan transaction. The lenders woo their consumers by offering higher repayment terms, lower interest rates and lower monthly instalments.

Tax Benefits on EMI’s

Under the secured loan category for certain loan product types there are reductions in tax on the monthly EMI’s. There are two types of people involved in getting this done, the lender and the tax consultant of the borrower. Under certain clauses the banks will be able to offer a tax rebate. It is recommended that the lender checks with their tax consultant before hand on this clause.

It is quite important that the lender plans before going ahead with a loan. Financial discipline is vital when it comes to using the loan acquired. Have a clear vision for what you need the loan, what type of loan and the advantages available in that loan that could be used towards your benefit. Try to make use of all the features and benefits of a loan against property so that you can save money and time.

FAQ’s

How many days will it take to get a LAP Sanctioned?

LAPs are sanctioned based on the property submitted. The property must be with clear title and accurate paper work. If all documents are in place one can get a LAP sanctioned in a week or two.

Are there differences in LAP based on Property location?

Yes, LAP – Loan against property can differ based on the location of the property. If a property is in a Prime Location of the city, then the value of the property can be much higher than a property in the outskirts. Based on the value of the property there can be differences in LAP.

Do banks accept un-registered properties for LAP?

As the name goes it is a Secured Loan and banks or NBFC’s don’t accept un-registered properties to offer loan against property. Banks can reject the loan application based on illegal documentation, litigation documentation and properties in disputes. So, when applying for a LAP please ensure that the property papers have a clear title.

When you are looking for a personal loan or a business loan you can consider attaching a property to the loan to reduce interest rates and increase tenure according to your repayment capacity. To begin with just understand in a simple way what is a LAP – Loan against property?

A loan against property is a loan that will be disbursed as a secured loan based on a property mortgaged by the borrower. The reason for taking the loan isn’t necessary to avail the loan. Before taking a loan against property it is advisable to make a thorough research or take the advice of a loan consultant who has good industry experience. You can carry out the research on your own by contacting lenders directly and collect Loan against property information.

First things first check your eligibility before approaching a lender. Eligibility criteria differs from one lending bank to another however there are some common eligibility checklists that you can prepare yourself with.

Eligibility Criteria Checklist

Be an Indian National. (Some banks & NBFC’s do accept NRI’s too)

A salaried or a self-employed person

Age is also a factor to be considered. (To calculate tenures and interest)

Must own a property (may be relaxed by some lending institutions)

Once you check your eligibility you will have to produce few documents for verification and the checklist is given below

Documents required for loan against property

Identity Proof of the individual applicant (Aadhar Card, Pan Card, Passport, Voter’s ID, Driver’s License)

Address Proof of the loan applicant (E.B Card or recent bill, Aadhar Card, Rental Agreement)

Documents of the Property Mortgaged (Original Sale Deed Document, NOC – No Objection Certificate from the local society), Possession document, Local Government Body Registration.

Proof of Income (Income tax certificate, salary slips, bank statements, P/L sheets, business registration certificates, GST certificate)

Now that you have understood the basic criteria and the documents required let’s understand the process of applying for a LAP – Loan against property

Process for applying for LAP – Loan against property

You can apply for a LAP from a bank, NBFC or through a loan consultant who can get you more choice of institutions.

If you go to a particular bank your choice is limited to the bank and it is the same with NBFC’s too, however if you get a loan consultant, they will go through your case specifically and apply in lending institutions that are likely to convert.

You can apply for a Loan Against Property by visiting the portal of a lending institution or the loan consultant. You can apply online and a team member will get in touch with you. In most cases the turn-around time will be 24 to 48 hours

A member from the lending team will go through your online application and schedule an appointment with you to collect documents for some banks and there are many institutions that do all transactions online itself.

The Online verification is quite easy when compared to meeting in person and it’s also quite fast.

The lending member will also allocate another member from the verification department to verify the property documents, visit the property and then finalize the amount of loan sanctioned accordingly.

Finally, if the application fits the bill and all criteria is met the LAP will be processed and sanctioned.

FAQ’s for Applying for a Loan Against property.

How long will it take to sanction LAP – Loan against property?

It may take any where between 30 to 60 days depending on the documents, property and other factors. There are various factors considered by banks in approving business loans and if all criteria are met then the loan may be disbursed quite earlier.

How to identify the best offers in the market for Loan against property?

Identifying which lending partner is offering the best loan offer is quite a difficult task for an individual to identify. The best thing to do is go with a loan consultant who are in partnership with banks, NBFC’s and other lending institutions.

Is there a standard interest rate for LAP – Loan against property?

No there isn’t a standard interest rate across all lenders. The interest rates depend on various factors. It comes in two types fixed interest rates and fluctuating interest rates.

There are humpty number of questions, doubts and series of little questions that pop up in the mind of a business owner who is looking for a Business Loan to improve his business. These questions arise out of fear of rejection of loan even before they can start thinking to apply. The success ratio of getting a loan for business approved quite easily depends on your preparedness and understanding of the requirements. In this article we outline a complete guide and handbook to loan against property for the year 2023-24 which can help you understand the requirements and rules involved. Let’s begin!

What is Loan Against Property?

The loan that you avail from a bank or a NBFC against a property that you own is called Loan against property. In banking terms, it is called mortgage loans where in you mortgage your property for an agreed and qualified sum of rupees for an agreed interest rate and loan repayment tenure. Property can be any registered one both commercial property of individual property. A loan against property can be availed for both personal reasons and business purpose too.

Now that you know what is a Loan against Property and what can you take it for, get to know other pointers about LAP

What is the sanctioned loan amount for Loan Against Property?

Sanctioned amount for LAP depends on various factor however the main criteria being the value of the property. The formula is 65% of the property value can be given as a loan amount however some banks and NBFC’s can extend the percentage up to 85% depending on the property value, its appreciation, repayment capacity, second line of income, investments and credit score. Based on the fulfilment of the criteria the lending institutions will approve the sanctioned loan amount.

Another important thing the lending institutions look in to is documents, let’s take a look.

List of required Documents for Loan Against Property

The very first and important document required for loan against property is the document of the property itself, showing ownership and legal correctness.

Followed by Identity proof, address proof, income proof, educational qualifications, proof of working in an organisation or proof of business in case of running a business, company registration certificate, GST certificate, bank statements and any other supporting documents that a lender may seek.

A processing fee will be levied in case of processing the loan by the lending institutions. Institutions in most cases deduct the processing fee from your loan amount and in some cases may collect it via check or online transfers after the loan is disbursed.

What is the rate of interest for LAP – Loan against Property?

Now, that’s a question where the answers differ from one lending institution to another. The rate of interest varies and is derived based on various factors. One cannot assume the rate of interest and it is advisable to take informed decisions when it comes to interest rates. Check, Compare and Continue with your loan if you are happy with the rate of interest.

Is there a fixed tenure for Loan Against Property?

The tenure of the loan purely depends on the amount, the monthly repayment capacity and maximum it can go up to 20 years as it even depends on the age of the applicant.

LAP – Loan against property vs Unsecured Business Loan

A simple comparison of LAP – Loan Against Property vs business loans or personal loans will give you a clear understanding on the different rates of interest on the loans. An unsecured loan be it for business or personal will definitely be high when compared to a LAP – Loan Against Property. Since the lending institution has a security with them in the form of a property the interest rates will be lower when compared to unsecured loans.

Summary

LAP – Loan against property is an easy approval loan from the lending institutions point of view as they know this is a secured loan. You will get a lower interest rate and longer tenure of repayment under the loan against property. Before applying for a Loan against please ensure you research well about the lending institutions offering various types of loans and schemes. It is highly advisable to have a loan consultant for your business loans and LAP’s. Prudent Capital has a team of experts who can offer expert advice, work on your account and turn your Loan against property dream in to a successful reality. With over 15+ years’ experience in the financial industry Prudent Capital can be your trusted Loan partner.

Faq’s on LAP – Loan against Property

Can an unemployed or retired person apply for Loan against property?

In such cases the banks or the NBFC’s will check for an income source in any form such as rent from property, pensions, FD’s and so on. If there is an income source it makes it easy for banks or lending institutions to offer a loan.

Can LAP – Loan against property be availed based on a Joint property?

One can surely get Loan against property approval in the case of joint property if both parties or all involved parties qualify as well as willing to pledge the property. All parties involved will have to sign the consent to mortgage the property. Joint acceptance of all the owners will be the important document for Loan Against Property in this case.

Are the interest rates fixed in Loan against property?

No, the interest rates are mostly on a variable or fluctuating interest rate model.

What is the time frame for approval on Loan against property?

It depends on the lending institutions and the documents presented too. On an average it may take a minimum of 20 business days.

Among these, unsecured business loans for women stand out as a beacon of support, offering capital without the burden of collateral.

In this comprehensive guide, we delve into the top business loans without collateral for women in India for the years 2023-24, providing a roadmap to turn entrepreneurial dreams into reality.

Mudra Loan: Empowering Entrepreneurs

At the forefront of government initiatives lies the Mudra Loan program, designed to fuel the aspirations of micro-enterprises. Launched in 2015 by the Honorable Prime Minister of India, this scheme extends unsecured business loans for women entrepreneurs, fostering financial inclusion and growth. With flexible repayment terms and competitive interest rates, Mudra Loan caters to startups and established ventures alike, empowering women to chart their own course in the business landscape.

Mahila Udhyam Nidhi Yojana: Nurturing Growth

The Mahila Udhyam Nidhi Yojana emerges as a catalyst for women-led businesses, offering working capital for income generation. Targeting new ventures, expansions, and modernizations, this government scheme provides collateral-free business loans to propel entrepreneurship among women. By facilitating access to funds and resources, it cultivates a conducive environment for women to thrive and contribute to the nation’s economic development.

Cent Kalyani Scheme: Driving Progress

In a bid to bolster women in business, the Central Bank of India introduced the Cent Kalyani Scheme, a testament to its commitment to female entrepreneurship. With minimal interest rates and comprehensive coverage across manufacturing and service sectors, this initiative enables women to kickstart or enhance their enterprises with ease. Whether it’s capital expenditure or day-to-day operations, the CKS scheme serves as a lifeline for MSME businesses owned by women.

Women Entrepreneur Development Scheme by TNSC Bank: Paving the Way

In collaboration with SIDBI, the Tamilnadu State Apex Co-operative Bank unveils a collateral-free loan scheme tailored to women entrepreneurs. Geared towards fostering self-employment and self-sufficiency, this scheme empowers educated women within Chennai Corporation limits to pursue their entrepreneurial aspirations. With a maximum sanction of Rs. 5 Lakhs and provisions for OD and term loans, TNSC Bank fuels the journey of women towards business success.

Bhartiya Mahila Bank Business Loan: Bridging Opportunities

Catering to economically underprivileged women, the Bhartiya Mahila Bank extends a helping hand through its business loan scheme. With a generous limit of up to Rs. 20 Crores, this initiative provides working capital, funds for manufacturing units, and support for business expansion. Setting the benchmark with competitive interest rates, BMB’s unsecured loans open doors for women to realize their entrepreneurial visions, backed by the assurance of CGTMSE coverage.

Conclusion

In the landscape of women’s entrepreneurship, collateral free business loan emerge as a vital tool for empowerment and growth. With a diverse array of schemes and initiatives, the Indian government and financial institutions pave the way for women to chart their own destinies in the business world. By harnessing the power of these loans, women entrepreneurs can seize opportunities, drive innovation, and carve out a niche for themselves in the dynamic realm of business.

Advantages and Disadvantages of Term Loans: What You Need to Know

These financial instruments have the potential to reshape growth trajectories and enhance financial stability for businesses. Imagine accessing a substantial injection of funds, complete with fixed interest rates for seamless financial planning and extended repayment periods for manageable cash flows. Term loans represent a gateway to financial empowerment, particularly advantageous for enterprises with strong credit scores.

In this detailed blog, we’ll take a close look at term loans. We’ll explore the advantages that can help your business, and we’ll also talk about the things you need to be careful about. Whether you’re someone experienced in business or just starting out, this guide will help you understand what term loans are all about.

What is a Term Loan? How does it work?

A term loan is a specific category of loan that involves repaying a predetermined sum of money over a specified period, usually spanning from 1 to 10 years. These loans are commonly utilized to finance substantial purchases, such as equipment or real estate.

The operational process of aterm loanis notably straightforward, once you acquire a designated sum from a lender, you undertake the responsibility of reimbursing this loan over a predefined period. This repayment is typically facilitated through regular, consistent monthly installments.

What distinguishes term loans is their fixed interest rate, which ensures predictability by allowing you to determine the exact interest amount payable each month. In essence, a term loan encapsulates a clear arrangement where you borrow a specific amount and then adhere to a structured timeline for its repayment, ensuring a systematic and predictable approach to settling the debt.

Advantages of Term Loans

Term loans stand as a pillar of financial support for businesses, offering a range of advantages that can redefine growth and stability. Let’s dive into these benefits to gain a comprehensive understanding of how term loans can empower your business’s financial journey.

Financial Flexibility and Stability Term loans introduce a sense of stability and predictability to your financial obligations. With a fixed repayment structure, you can precisely determine your monthly payments, streamlining budgeting and cash flow management. This foresight extends to long-term planning, allowing you to harmonize business strategies with financial commitments. This dual sense of stability collectively fosters business growth and equilibrium.

Lower Interest Rates Term loans offer the advantage of cost-effective borrowing, particularly for loans backed by collateral. Collateralized loans, where you provide assets as security, often result in more favorable interest terms due to perceived lower risk for lenders. Furthermore, fixed interest rates serve as a safeguard against market rate volatility, simplifying financial projections and eliminating uncertainty about future borrowing costs.

Access to Larger Capital Term loans serve as a gateway to substantial capital, rendering them ideal for ambitious undertakings. Whether your focus is expansion, embarking on significant ventures, or making substantial asset investments, term loans equip you with the financial means to seize opportunities that might otherwise remain elusive. This capacity to access larger capital positions your business to thrive on a more expansive scale.

Diversified Use A core strength of term loans lies in their adaptability. Unlike financing options with imposed usage limitations, term loans empower you to allocate funds as per your specific business needs. Whether addressing challenges, pursuing avenues for growth, or enhancing operational capabilities, term loans deliver the financial versatility necessary to navigate dynamic market conditions.

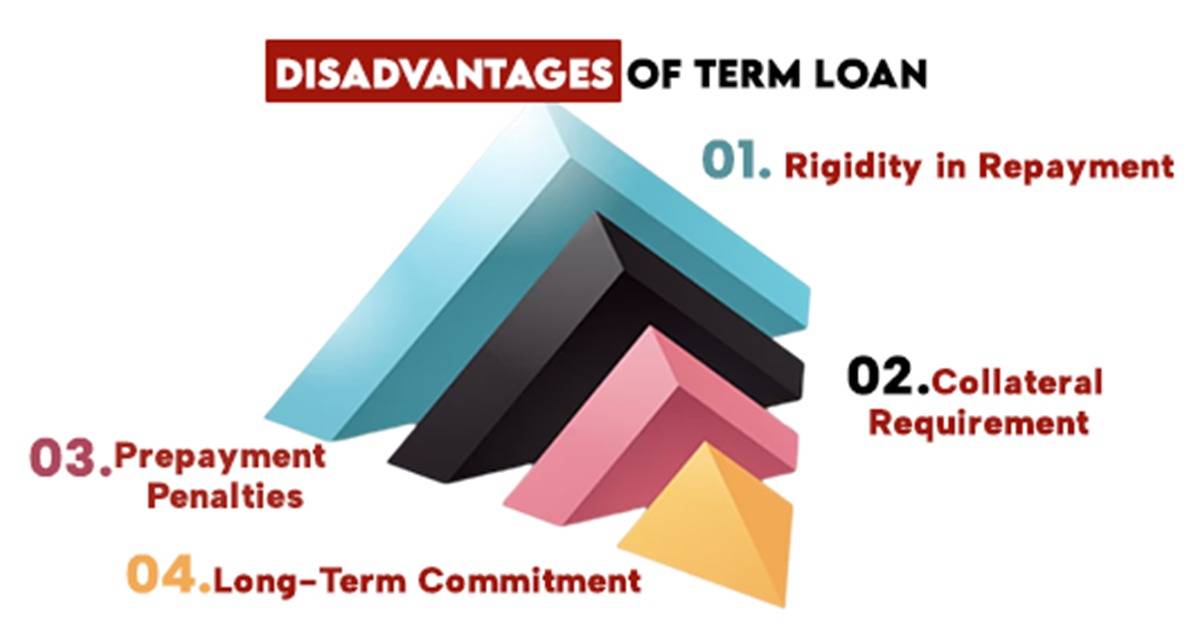

Disadvantages of Term Loan

As we explore the pros of term loans, it’s essential to recognize the potential challenges that can accompany these financing options. Here’s a closer look at these disadvantages, shedding light on the considerations that businesses should be mindful of:

A. Rigidity in Repayment

The structured nature of term loan repayments, while aiding in financial planning, can also introduce rigidity. This fixed repayment schedule might become a challenge if unexpected financial fluctuations occur, as adapting repayment schedules accordingly might not be feasible. Furthermore, the consistency of fixed monthly payments can strain cash flow, particularly during periods of financial tightness. This rigidity necessitates careful budgeting to ensure consistent meeting of financial obligations.

B. Collateral Requirement

Term loans often require collateral, which can present potential disadvantages. While collateralization can secure lower interest rates, the risk lies in the possibility of asset seizure in case of loan default. Pledging valuable assets as collateral can also impact your business’s asset portfolio, potentially limiting its usability for other financial opportunities.

C. Prepayment Penalties

Term loans might come with prepayment penalties if you choose to pay off the loan ahead of schedule. While intended to ensure lenders earn expected interest, these penalties can complicate early loan repayment. Weighing potential cost savings on interest against prepayment penalties becomes a crucial factor when considering paying off the loan before its term.

D. Long-Term Commitment

Opting for a term loan commits your business to a long-term financial arrangement. While this might suit certain needs, it can potentially impact business flexibility. Tied-up cash flow and financial capacity might hinder your ability to swiftly respond to unforeseen opportunities or challenges. Moreover, committing to a long-term loan might not align with potential shifts in your business’s strategic direction.

In essence, while term loans offer various advantages, understanding these potential disadvantages is equally vital. This comprehensive perspective empowers businesses to make informed financial decisions that align with their unique circumstances and aspirations.

Summary

Term loans stand as a dual-edged sword, offering a robust array of advantages that can propel your business to new heights, while also presenting potential challenges that require careful consideration. As you traverse the landscape of financing options, arming yourself with knowledge about the pros and cons of term loans is a strategic move.

Ultimately, the journey of business financing is about achieving an equilibrium between aspiration and caution. Term loans, when embraced with prudence and foresight, can be a pivotal driver in propelling your business toward its goals, fortifying financial health, and ensuring a dynamic and sustainable future.j